Corporate tax rates are a pivotal point of debate among policymakers and economists, especially as the 2017 Tax Cuts and Jobs Act (TCJA) approaches its critical expiration date. With the next congressional session looming, discussions about whether to maintain or increase these rates are intensifying. Recent analysis by Harvard macroeconomist Gabriel Chodorow-Reich offers insight into the effects of the TCJA on corporate tax revenue and economic growth. Despite initial claims of tax cuts spurring investment, Chodorow-Reich’s findings suggest that the tangible benefits were not enough to counterbalance a significant decline in tax income. As Americans ponder the future of corporate taxation, understanding the implications of these policies on revenue and economic health is more essential than ever.

When examining the landscape of corporate taxation, the discussion often hinges on the fiscal consequences of adjusting corporate income taxes. As legislators prepare for significant tax reforms, the focus shifts towards how changes in tax policy can affect business operations and governmental revenue streams. Research, including that by economist Gabriel Chodorow-Reich, sheds light on the complex interactions between corporate tax structures and overall economic vitality. This includes contributions from the 2017 Tax Cuts and Jobs Act, which aimed to reshape the corporate tax system dramatically. Analyzing the expiration of various tax provisions reveals critical insights into how adjustments can influence investment, wages, and ultimately, the nation’s financial health.

The Impact of the Tax Cuts and Jobs Act on Corporate Tax Rates

The Tax Cuts and Jobs Act (TCJA), enacted in 2017, brought significant changes to corporate tax rates in the United States, lowering them from 35% to 21%. This reduction was aimed at increasing competitiveness in a global market that saw many other countries cutting their rates. The expectation was that such a substantial cut would stimulate economic growth by encouraging business investment and driving up wages. However, analysis by economists like Gabriel Chodorow-Reich indicates a more nuanced picture, suggesting that while some investments did increase, the overall impact on corporate tax revenue has not been as favorable as proponents of the TCJA had anticipated.

Chodorow-Reich’s research indicates that the immediate aftermath of the TCJA was a dramatic drop in corporate tax revenue, initially plummeting by 40%. This decline was a major topic of discussion during recent political debates, as both parties grapple with the implications of these tax cuts. While some argue for further reductions in corporate tax rates to spur economic growth, others advocate raising them to restore lost revenue and address budget shortfalls from expiring provisions. As the expiration of several key elements of the TCJA approaches in 2025, the discussion on how to balance corporate tax rates remains contentious.

Evaluating the Effect of Expiring Provisions on Economic Growth

As portions of the TCJA begin to expire, particularly those aimed at boosting family income like the Child Tax Credit, the debate intensifies around which provisions have contributed most effectively to economic growth. The research from Chodorow-Reich points to certain expiring provisions as having had significant positive effects, particularly those allowing for immediate expensing of capital investments. These temporary tax incentives encouraged businesses to invest in new technologies and equipment, thereby creating jobs and, ultimately, contributing to wage growth.

Conversely, the expiration of such provisions could have a detrimental effect if companies decide to scale back on investments due to increased uncertainty. The debate often centers around the need for incentives that directly contribute to tangible economic benefits rather than solely focusing on corporate tax rate reductions. Discussions around potential solutions include reinstating these expired provisions while considering a reasonable increase in corporate tax rates to balance budgetary needs and economic growth.

Lessons from the 2017 Tax Cuts: Corporate Tax Revenue Trends

The aftermath of the Tax Cuts and Jobs Act offers important lessons about corporate tax revenue trends in relation to economic behavior. Initially, the corporate tax revenue saw a sharp decline, causing concern among economists and policymakers alike. However, an unexpected rebound began around 2020, bringing corporate tax revenues back up significantly as businesses adapted to new economic conditions during the pandemic. Chodorow-Reich’s analysis indicates that this rebound was largely driven by greater-than-expected business profits, which defied earlier forecasts of stagnant or declining corporate income.

This raises critical questions about the underlying factors that influence corporate decision-making and tax strategy. The surge in corporate profits during a time of economic uncertainty highlights the importance of examining how tax policies and market conditions interact. It suggests that a comprehensive approach toward tax reform, which takes into account both the benefits of lowering rates and the necessity for adequate revenue, is essential for sustainable economic growth.

The Role of Partisan Debate in Corporate Tax Policy

As 2025 approaches, the partisan debate surrounding corporate tax policy has intensified, with each party positioning itself based on the perceived successes or failures of the TCJA. Democrats, led by figures like Kamala Harris, are advocating for increasing corporate tax rates as a means to fund social initiatives and restore fiscal balance, while Republicans emphasize the need to maintain or reduce rates to further encourage economic growth. This partisan division often oversimplifies complex economic realities, as highlighted in Chodorow-Reich’s work, which calls for a more nuanced understanding of how tax policy impacts growth and investment.

The polarization surrounding corporate tax rates can lead to inconsistent policy-making that may undermine investor confidence and economic stability. Economists argue that moving beyond simple partisan talking points is essential for creating policies that effectively drive economic growth while ensuring adequate revenue collection. Constructive dialogue that acknowledges multiple facets of tax reform could propose alternatives that resonate with both sides, potentially resulting in solutions that balance the need for business investment incentives and necessary public funding.

Research Insights on Corporate Taxation and Investment Rates

Gabriel Chodorow-Reich’s research sheds valuable light on the relationship between corporate tax rates and business investment decisions. His findings indicate that while lower corporate tax rates have been shown to stimulate some degree of investment, the most impactful elements of the TCJA were actually the expensing provisions that expired recently. By allowing businesses to deduct the full cost of capital investments immediately, firms were incentivized to allocate funds toward growth, leading to increased economic activity.

This research challenges the narrative that simply lowering tax rates is sufficient to drive substantial investment. Rather, it suggests that the structure of tax incentives plays a crucial role in defining corporate behavior. As discussions about future tax policy continue, it is essential for lawmakers to consider both the tax rate and the type of incentives created to ensure that they foster sustainable growth in the corporate sector while maintaining the integrity of public finances.

Prospects for Future Tax Provisions and Economic Strategies

Looking to the future, there is a pressing need for reevaluation and possibly restructuring of tax provisions as key elements of the TCJA are set to expire. Effective economic strategies will depend not only on adjusting corporate tax rates but also on understanding broader influences such as global market trends, domestic business sentiments, and public expectations regarding taxation. Chodorow-Reich’s research highlights the importance of temporary incentives and how their design can significantly impact overall economic growth.

Congress faces a critical opportunity to reassess what tax policies work best in cultivating investment and supporting wage growth. As the current political climate remains highly polarized, there exists a challenge in crafting solutions that satisfy both fiscal responsibility and the need for ongoing economic stimulation. Constructive policy discussions that include the perspectives of economists, corporations, and the public will be vital in determining the future landscape of corporate taxation.

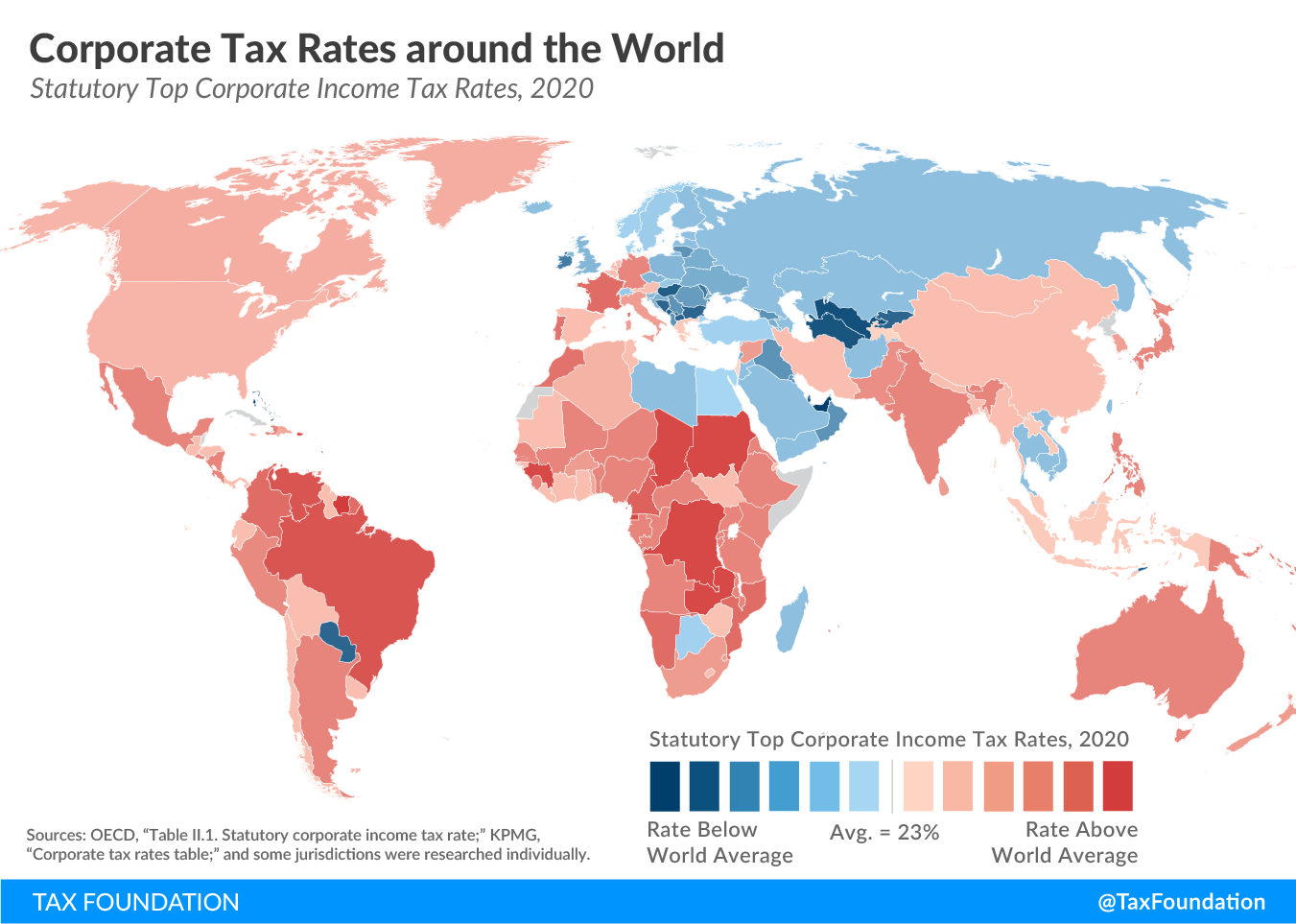

Global Comparisons in Corporate Tax Rates and Strategies

In an increasingly globalized economy, the comparison of U.S. corporate tax rates to those of other countries is more pertinent than ever. Gabriel Chodorow-Reich emphasizes that prior to the TCJA, the U.S. had the highest corporate tax rates among developed nations. This unsustainable position prompted necessary reform but also set the stage for heated debate over the effectiveness of further tax reductions. Understanding how international competition influences U.S. tax policy is crucial for future legislative discussions.

As countries around the world reconsider their corporate tax strategies, the U.S. needs to keep pace to ensure it is not left at a competitive disadvantage. Significant shifts, such as Ireland’s changes to its previously ultra-low corporate tax rates, have started redirecting corporate profits back to the U.S. This illustrates the interconnectedness of global tax policies and the necessity of implementing thoughtful reforms that prevent capital flight while encouraging both investment and revenue generation.

Balancing Corporate Tax Increases with Economic Growth Initiatives

As the deadline for expiring provisions draws nearer, the conversation becomes increasingly focused on striking the right balance between raising corporate tax rates and fostering economic growth. Some economists believe that increasing corporate rates could provide essential revenue without significantly hampering business investment, especially if coupled with retained expensing provisions. This approach aims to cater to both sides of the political spectrum by ensuring that corporations are contributing their fair share while still being incentivized to reinvest in growth.

Chodorow-Reich’s findings support a middle-ground strategy where lawmakers consider incremental changes rather than drastic cuts or hikes in corporate taxes. Policymakers may consider partially reversing the TCJA’s rate reductions while simultaneously reinstating expired incentives. This dual approach could lead to a rejuvenation of corporate tax revenues while preserving business investment momentum that could contribute to higher wage growth and more robust economic activity in the long term.

The Future of Tax Legislation and the Economic Landscape

With the impending expiration of key tax provisions, the landscape for future tax legislation is uncertain but ripe for reform. Lawmakers are tasked with finding solutions that address both immediate fiscal needs and longer-term economic strategies. Chodorow-Reich’s research emphasizes the necessity of data-driven approaches to reform, allowing for decisions that are informed by empirical evidence of how past tax policies have influenced corporate investment and growth.

As both sides of the political aisle prepare for negotiations, establishing a common understanding of the realities faced by businesses under current tax arrangements will be vital. Instead of allowing partisan divides to cloud the conversation, a collaborative effort focused on pragmatic reform could lead to legislation that supports economic resilience and equitable tax contributions from corporate entities, paving the way for a more stable economic future.

Frequently Asked Questions

What impact did the 2017 Tax Cuts and Jobs Act have on corporate tax rates?

The 2017 Tax Cuts and Jobs Act (TCJA) significantly reduced the corporate tax rate from 35% to 21%. This change aimed to stimulate economic growth by providing financial relief to corporations, encouraging them to invest more and hire additional employees.

How have corporate tax rates influenced corporate tax revenue since the TCJA?

Since the implementation of the TCJA, corporate tax revenue initially fell by about 40%. However, it began to rebound starting in 2020 as business profits rose unexpectedly, surpassing initial forecasts.

What does Gabriel Chodorow-Reich’s research say about corporate tax cuts and economic growth?

Gabriel Chodorow-Reich’s research indicates that while the TCJA led to increased capital investments by about 11%, the anticipated wide-ranging economic growth and significant wage increases have not materialized to the extent predicted, suggesting a more complex relationship between corporate tax rates and economic performance.

Are there expiring provisions related to corporate tax rates from the TCJA that should be renewed?

Yes, several provisions from the TCJA aimed at expensing investments are set to expire soon. Chodorow-Reich’s analysis suggests that these provisions have been more effective at driving investment than traditional rate cuts, indicating they might be worth renewing as part of any tax reforms.

What are the differing opinions on raising corporate tax rates in the current economic climate?

Opinions vary: some, including Kamala Harris, argue for raising corporate tax rates to fund initiatives, while others, like Donald Trump, advocate for further cuts to stimulate economic growth. Gabriel Chodorow-Reich’s research provides evidence that corporate tax policy does influence business behavior, which complicates these narratives.

How do corporate tax rates affect wages in the long term?

Corporate tax rates can indirectly impact wages; as companies invest more due to lower tax rates, they may need to hire additional workers, potentially driving up wages. However, findings from Chodorow-Reich suggest any wage increases have been modest, leading to ongoing debate about the effectiveness of tax cuts in raising income levels.

What lessons can we learn from the corporate tax rate changes under the TCJA?

The experience with corporate tax rates post-TCJA highlights the need for a balanced approach that considers both the benefits of lower rates for business growth and the consequences on corporate tax revenue. Effective tax reforms may require a combination of adjustments, such as raising rates while reinstating beneficial expensing provisions.

Why did corporate tax revenue plummet initially after the TCJA was enacted?

The sharp decline in corporate tax revenue following the enactment of the TCJA can be attributed to the significant reduction in the corporate tax rate, which lowered the taxes owed by corporations. This led to a temporary shortfall in government revenue until business profits began to increase again.

| Key Points |

|---|

| Tax reform anticipated in 2025 as parts of the TCJA expire. |

| Debate over whether to raise or lower corporate tax rates continues. |

| Chodorow-Reich’s study indicates modest wage increases and investment under TCJA. |

| Corporate tax revenue fell by 40% after TCJA but began to rebound in 2020 due to higher business profits. |

| Investment increased by roughly 11%, indicating tax policy impacts business decisions. |

| Raising statutory tax rates while reinstating expensing provisions could be a beneficial compromise. |

| Wage increases following TCJA were lower than initially predicted, averaging around $750 per year. |

Summary

Corporate tax rates have become a hot topic as Congress prepares for a new tax debate in 2025. The expiration of key provisions from the 2017 Tax Cuts and Jobs Act (TCJA) sets the stage for discussions on whether to raise or cut corporate tax rates further. Gabriel Chodorow-Reich’s recent research provides valuable insight into the effects of the TCJA, indicating that while investments and wages saw some increases, the overall impact was not as substantial as advocates had suggested, and corporate tax revenues initially fell significantly. As lawmakers consider their options, finding a balance that encourages investment while ensuring adequate revenue will be crucial.